A 15-year loan will pay off your house in half the amount of a 30-year loan. Other advantages of a 15-year mortgage are that it will have a lower LLPA and will help you build equity quicker. A 30-year loan may be easier to manage if you have additional financial goals.

A 15-year mortgage is half the time to pay off your home than a 30-year.

A 15-year term mortgage is an option for people who are looking to reduce their time in paying off their homes. A 15 year mortgage will give you the opportunity to build equity faster, and decrease your monthly expenses. You can also get a loan or credit line to help you pay down your home equity, so you can own it sooner.

While the monthly payment on a 15-year mortgage will be higher than a 30-year mortgage, it may be worth it if it fits into your housing budget and your income has increased. You may also want to prequalify for a loan if you are interested in a 15-year mortgage due its lower interest rates. This will allow to compare 15 year mortgage rates from different lenders.

Lower LLPA

The cost of home loans is more expensive for a 15 year fixed-rate mortgage than a 30 year fixed-rate mortgage. The reason is that 15 year fixed-rate loans are exempt from loan price adjustments. These increases add up to a 30-year fixed interest mortgage. The fees for 15-year fixed rates mortgages are lower than those for 30-years.

The advantage of a 15-year mortgage is the speed with which equity can be built. With a 15-year loan, you'll build equity faster, which is important if you want to take out a home equity loan or a home equity line of credit. A 15-year mortgage will allow you to make higher monthly principal payments, which will help build equity faster.

Despite its benefits, the LLPA has some drawbacks. Lenders face greater risk if there is a higher LLPA. Second, a higher LLPA will make it harder for American families to buy homes. LLPA can be described as a risky mortgage that puts homeownership out of reach of many families.

Increases equity quicker

A 15-year term mortgage will help you build equity faster than a 30 year mortgage. This is due to the shorter term and lower interest rate. Many people with a 30-year-old mortgage would have been better off with an adjustable rate mortgage. For the shorter term, however, you'll have to make higher payments. It is up to you to decide if you want to pay your loan off as quickly as possible, or maximize your wealth.

A 15-year term mortgage typically has a lower monthly payment, as well as a lower interest rates than a 30-year. The lower interest rate can help build equity quicker and reduce your total mortgage debt. The 15 year mortgage will also help you build equity faster so you can refinance/sell your home sooner.

FAQ

Which is better, to rent or buy?

Renting is typically cheaper than buying your home. It is important to realize that renting is generally cheaper than buying a home. You will still need to pay utilities, repairs, and maintenance. Buying a home has its advantages too. You will have greater control of your living arrangements.

What is a reverse loan?

A reverse mortgage allows you to borrow money from your house without having to sell any of the equity. You can draw money from your home equity, while you live in the property. There are two types to choose from: government-insured or conventional. With a conventional reverse mortgage, you must repay the amount borrowed plus an origination fee. FHA insurance covers repayments.

Can I get another mortgage?

However, it is advisable to seek professional advice before deciding whether to get one. A second mortgage can be used to consolidate debts or for home improvements.

Is it possible to quickly sell a house?

If you have plans to move quickly, it might be possible for your house to be sold quickly. Before you sell your house, however, there are a few things that you should remember. First, you must find a buyer and make a contract. Second, prepare the house for sale. Third, you need to advertise your property. You should also be open to accepting offers.

What are the most important aspects of buying a house?

The three main factors in any home purchase are location, price, size. Location refers to where you want to live. Price refers how much you're willing or able to pay to purchase the property. Size refers to the space that you need.

Statistics

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

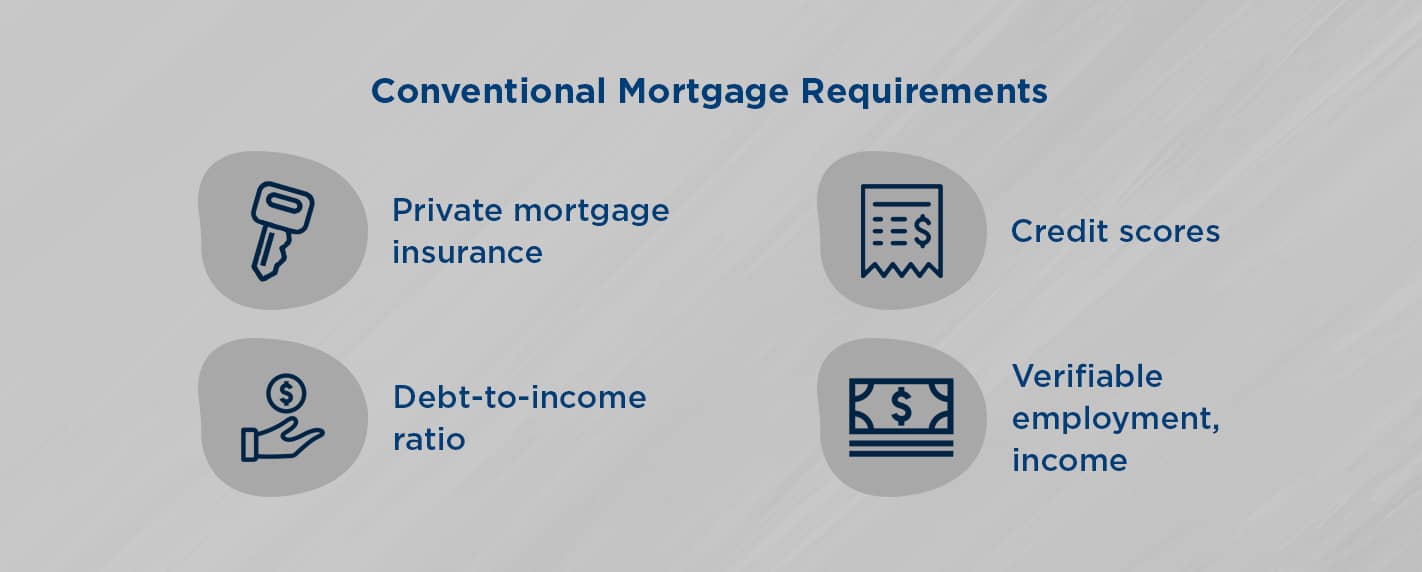

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

External Links

How To

How to Buy a Mobile Home

Mobile homes are houses that are built on wheels and tow behind one or more vehicles. They have been popular since World War II, when they were used by soldiers who had lost their homes during the war. People who want to live outside of the city are now using mobile homes. These houses are available in many sizes. Some houses have small footprints, while others can house multiple families. Even some are small enough to be used for pets!

There are two types main mobile homes. The first type is produced in factories and assembled by workers piece by piece. This is done before the product is delivered to the customer. You can also build your mobile home by yourself. It is up to you to decide the size and whether or not it will have electricity, plumbing, or a stove. You'll also need to make sure that you have enough materials to construct your house. You will need permits to build your home.

You should consider these three points when you are looking for a mobile residence. You may prefer a larger floor space as you won't always have access garage. Second, if you're planning to move into your house immediately, you might want to consider a model with a larger living area. Third, make sure to inspect the trailer. If any part of the frame is damaged, it could cause problems later.

Before you decide to buy a mobile-home, it is important that you know what your budget is. It is important that you compare the prices between different manufacturers and models. Also, take a look at the condition and age of the trailers. While many dealers offer financing options for their customers, the interest rates charged by lenders can vary widely depending on which lender they are.

Instead of purchasing a mobile home, you can rent one. Renting allows the freedom to test drive one model before you commit. Renting is not cheap. Renters generally pay $300 per calendar month.