A share equity loan has many benefits. One advantage is that you can make your payments more easily and you can pay the loan off in shorter terms. The loan provider may also offer incentives for early repayment, such as a short settlement period. These can be very helpful to borrowers who are selling their property in a hurry.

Equity loan for homeowners

A house equity loans is a type home loan you can use to make renovations to your home. These improvements can improve the value of your home and your quality of living. The money can also be used to consolidate your debt. This can help you save money in the long term. You will need to know how much you owe, and what interest rate you will get on your home equity loan.

You can apply online for household equity loans, which are typically between $35,000 to $150,000. HELOCs are available from many banks for primary residences. Many offer reductions in charge to existing customers. Citibank allows you to apply online and by phone. There are no application or closing fees. However, annual fees might apply to the loan.

HELOC or Household Equity Loan

The interest rate is what makes a home equity loan different from a home equity credit line. A home equity loan will have a fixed interest rate while a HELOC rate can change over time. In the event that the interest rate goes up, you may have a higher monthly repayment. Some lenders offer HELOC rate lock options. These typically have higher interest rates, and additional fees.

HELOCs are a second mortgage that allows the borrower to use their equity as a line credit. They are able to borrow as much or as little as they want, depending on the lender's limits. They can be used for home improvements, college education, or consolidating credit card debt.

HELOCs typically have a draw period that lasts ten years. After the draw period ends, the loan enters a repayment period during which the borrower must pay the outstanding balance. The repayment period can be up to 20 years. HELOC interest rates are determined by the lender, borrower's credit score and amount borrowed.

Comparing house equity loan and share equity loan

These secured loans can be taken out against your home as a household equity loan. These loans come with a downside: your home may be at risk if they aren't paid on time. Before you apply, it is essential to create a plan of repayment. A household equity loan will help you pay off debts and get cash for retirement.

These loans offer lower risk and are attractive options. In a down market, they can offer lower monthly payments. Furthermore, the flexibility of shared equity loans allows for a greater down payment.

You will also see a difference in how the cash is received between a equity loan and home equity loans. You can use a home equity loan to pay one lump sum for large expenses, such as home renovations or debt consolidation. These loans have a long repayment term and low interest rates. This can increase your cash flow.

FAQ

How do I fix my roof

Roofs can become leaky due to wear and tear, weather conditions, or improper maintenance. Minor repairs and replacements can be done by roofing contractors. Get in touch with us to learn more.

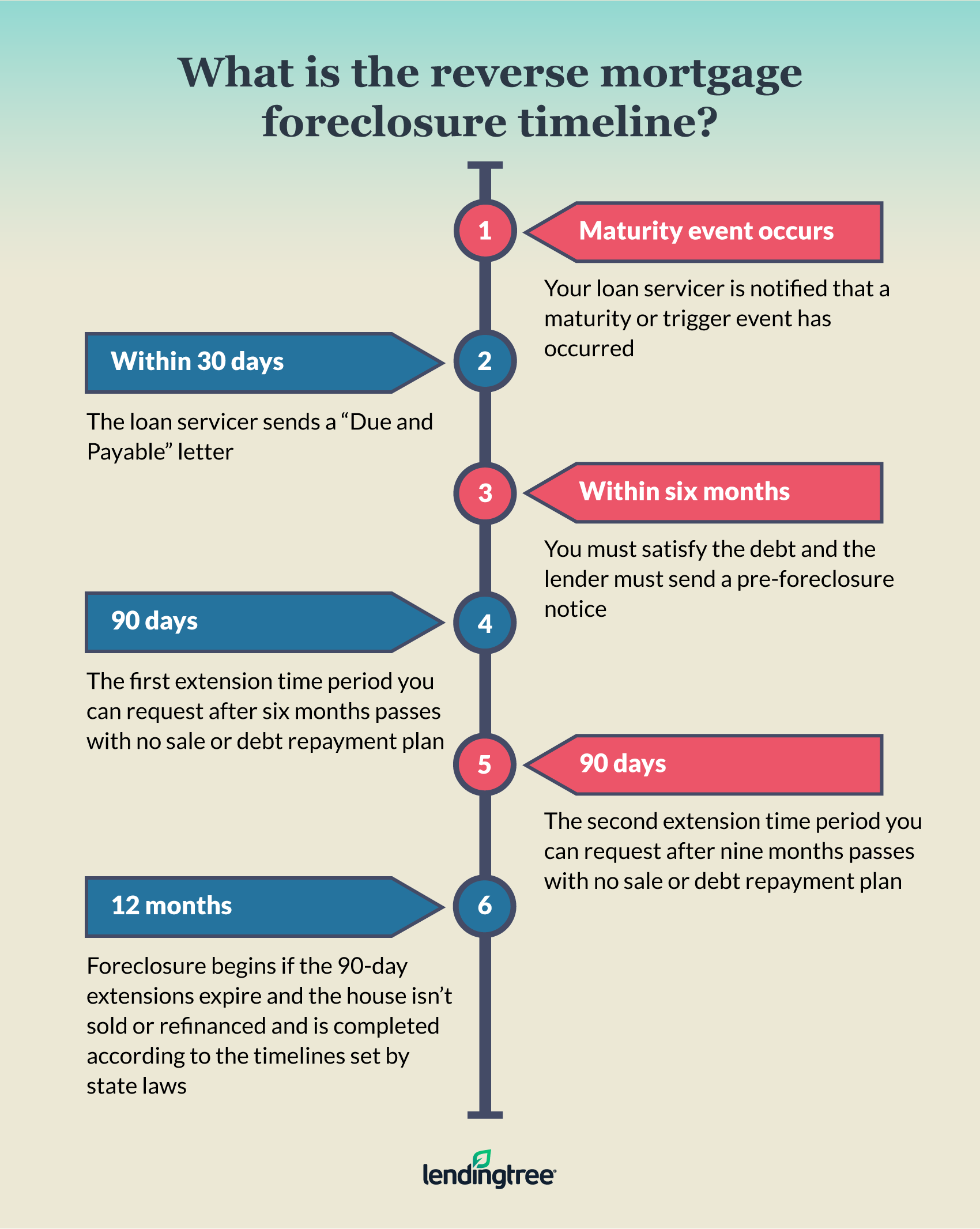

What is reverse mortgage?

A reverse mortgage allows you to borrow money from your house without having to sell any of the equity. It allows you to borrow money from your home while still living in it. There are two types: government-insured and conventional. You must repay the amount borrowed and pay an origination fee for a conventional reverse loan. FHA insurance covers the repayment.

Should I use a mortgage broker?

A mortgage broker can help you find a rate that is competitive if it is important to you. Brokers work with multiple lenders and negotiate deals on your behalf. However, some brokers take a commission from the lenders. Before you sign up for a broker, make sure to check all fees.

Statistics

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

External Links

How To

How to Buy a Mobile Home

Mobile homes can be described as houses on wheels that are towed behind one or several vehicles. Mobile homes have been around since World War II when soldiers who lost their homes in wartime used them. Mobile homes are still popular among those who wish to live in a rural area. There are many options for these houses. Some houses can be small and others large enough for multiple families. You can even find some that are just for pets!

There are two main types mobile homes. The first is built in factories by workers who assemble them piece-by-piece. This happens before the product can be delivered to the customer. You could also make your own mobile home. You'll need to decide what size you want and whether it should include electricity, plumbing, or a kitchen stove. Next, ensure you have all necessary materials to build the house. The permits will be required to build your new house.

These are the three main things you need to consider when buying a mobile-home. You might want to consider a larger floor area if you don't have access to a garage. A model with more living space might be a better choice if you intend to move into your new home right away. The trailer's condition is another important consideration. Problems later could arise if any part of your frame is damaged.

Before buying a mobile home, you should know how much you can spend. It is important that you compare the prices between different manufacturers and models. Also, consider the condition the trailers. Although many dealerships offer financing options, interest rates will vary depending on the lender.

Instead of purchasing a mobile home, you can rent one. You can test drive a particular model by renting it instead of buying one. Renting is expensive. Renters generally pay $300 per calendar month.