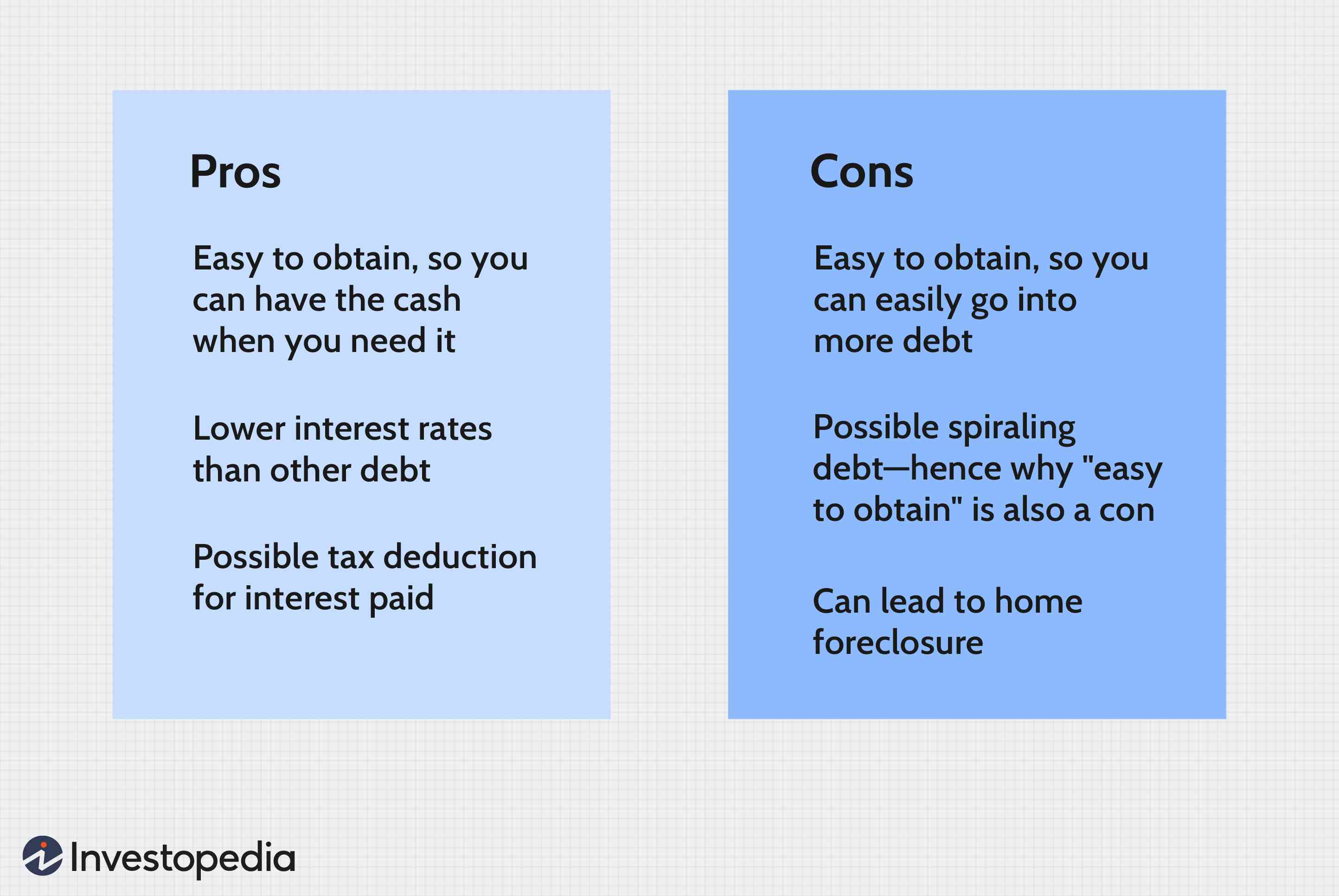

Virginia refinance rates can be tailored to your down payment, credit score, and loan program. These rates are available for many types of home loan and are constantly updated. These rates include the lender fees and the interest rate. You can determine which loan is right for you by looking at the annual percentage rate (APR).

Virginia mortgages are deeds-of-trust.

Mortgages and trust deeds are two different types. To secure loans, trust deeds are used. These types of contracts are governed by state law. Some states allow only one type, while others allow both. Lenders can choose which type of contract is best for them. Others do not recognize deeds to trust or mortgages and instead use other types such as security documents.

A mortgage is a secured real property transaction that involves more than one party. Through a promissory notice, the lender and borrower exchange cash. The borrower then transfers the property's interests to a third party trustee. The trustee can then take title to the property if the borrower doesn't pay off the loan.

Lenders take on greater risk with jumbo loans

While jumbo loan have many benefits, they are more risky for lenders. These loans are more risky than conventional mortgages because they require higher down payments and income requirements. They also have higher interest rate potential. These loans are more risky and require more documentation and paperwork in order to be approved. You can negotiate for better terms for the borrower.

Prepare your financial picture before you apply to a loan jumbo. All financial documents should be gathered and copies of credit reports requested. You can review your credit scores to determine if the monthly payments are feasible. Collect copies of any personal identification documents, bank statements or pay slips.

VA loans are subject to a 12-month waiting period

Before you apply for a VA loan, be sure to consider the time frame involved. Most loans require at least a 12-month waiting period. Depending on your personal circumstances, this time period could be shorter or more. During this period, the VA will examine your payment history for the last year. If you have had a poor payment history in the past, you can be forgiven if you can prove that your past payments were due to active-duty deployments or disability-related health challenges. The VA is very sensitive to these situations.

VA loans can be beneficial to veterans and active-duty personnel. There are no down payment requirements, no prepayment penalties, low closing costs and no loan limits. You may not be eligible if bankruptcy has been filed within the last 2 years. A stable credit score and proof that you can afford repayments are essential.

VA IRRRL program results are a brand new raw loan

VA IRRRL loans are designed to simplify the refinancing process. The program offers VA benefits to borrowers and makes it more affordable. However, not all VA benefits can be utilized with this program. Consider another option if you are a military veteran or servicemember. The VA IRRRL does not require income verification nor credit checks.

A Certificate of Eligibility (COE), is necessary to be eligible for IRRRL. The VA portal allows you to electronically obtain your Certificate of Eligibility (COE). In addition, you will need to pay closing costs and fees. In certain instances, you will need to pay a VA fund fee. This fee reduces the cost to get a VA mortgage for U.S. citizens. VA home loans are free from down payments and monthly mortgage insurance. However, interest will still be charged on the loan.

The interest rates for ARMs are not subject to change

An ARM can be a mortgage that has a variable interest rate. It may be fixed for a certain time or may move with the market. An ARM consists two parts. The index rate and margin. The market rate is used to determine the index rate. The loan's term will determine the margin.

The qualification criteria for the new ARM are important if you want to modify the interest rates on your mortgage. VA ARMs can be flexible and don't require a downpayment. There are limitations on the maximum interest rate that can be charged.

FAQ

What are the three most important things to consider when purchasing a house

Location, price and size are the three most important aspects to consider when purchasing any type of home. Location refers to where you want to live. Price refers how much you're willing or able to pay to purchase the property. Size refers to the space that you need.

What is a "reverse mortgage"?

Reverse mortgages allow you to borrow money without having to place any equity in your property. It allows you to borrow money from your home while still living in it. There are two types available: FHA (government-insured) and conventional. Conventional reverse mortgages require you to repay the loan amount plus an origination charge. FHA insurance covers repayments.

What are the benefits associated with a fixed mortgage rate?

Fixed-rate mortgages lock you in to the same interest rate for the entire term of your loan. You won't need to worry about rising interest rates. Fixed-rate loans come with lower payments as they are locked in for a specified term.

How long does it take for my house to be sold?

It all depends upon many factors. These include the condition of the home, whether there are any similar homes on the market, the general demand for homes in the area, and the conditions of the local housing markets. It can take from 7 days up to 90 days depending on these variables.

Which is better, to rent or buy?

Renting is typically cheaper than buying your home. It's important to remember that you will need to cover additional costs such as utilities, repairs, maintenance, and insurance. Buying a home has its advantages too. You will be able to have greater control over your life.

Statistics

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

External Links

How To

How to locate an apartment

Moving to a new place is only the beginning. This process requires research and planning. This includes researching the neighborhood, reviewing reviews, and making phone call. There are many ways to do this, but some are easier than others. Before renting an apartment, you should consider the following steps.

-

Researching neighborhoods involves gathering data online and offline. Online resources include websites such as Yelp, Zillow, Trulia, Realtor.com, etc. Local newspapers, real estate agents and landlords are all offline sources.

-

You can read reviews about the neighborhood you'd like to live. Yelp. TripAdvisor. Amazon.com all have detailed reviews on houses and apartments. You can also check out the local library and read articles in local newspapers.

-

For more information, make phone calls and speak with people who have lived in the area. Ask them what they liked and didn't like about the place. Also, ask if anyone has any recommendations for good places to live.

-

You should consider the rent costs in the area you are interested. Renting somewhere less expensive is a good option if you expect to spend most of your money eating out. On the other hand, if you plan on spending a lot of money on entertainment, consider living in a more expensive location.

-

Find out about the apartment complex you'd like to move in. How big is the apartment complex? How much is it worth? Is it pet-friendly? What amenities is it equipped with? Is it possible to park close by? Are there any rules for tenants?