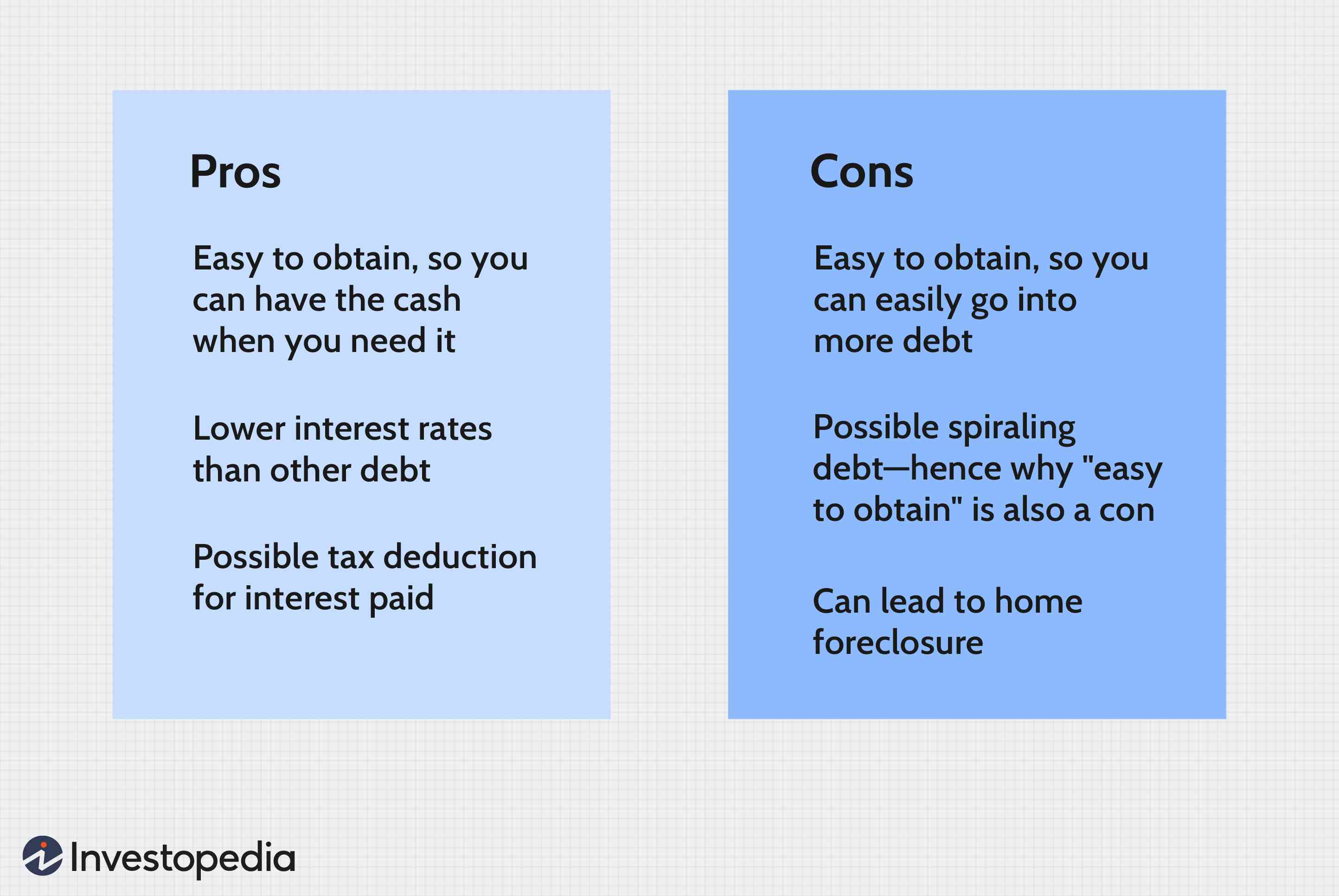

A HELOC is a loan that allows you to borrow the maximum amount for your home. This loan allows you borrow the maximum amount for a given time. Your home's equity will secure the money you borrow. Before you apply for a HELOC you need to know what the lender expects of you. A home appraisal may be required if there isn't enough equity.

Getting a heloc

Knowing what to expect during the application process for a HELOC is essential. HELOCs use your home equity as collateral. Lenders will usually lend you the maximum amount within a given time period. It is important that you understand what this type a loan is and how to get the best deal. Many people ask if they will need a HELOC appraisal.

A HELOC appraisal can show the lender what your house is worth. The lender must know the amount of equity and owes against it. Getting a home equity appraisal is an important step for any home loan process. It protects both the borrower, and the lender.

Getting a second mortgage

A second mortgage is a great way to borrow against your home's equity, but there are several factors to consider before applying for one. An appraisal of your equity will be required by the lender to determine how important it is for the lending process. This document will show how much equity you have in your home, as well as what the loan will be worth.

Lenders will also be interested in your credit score. The lender will look at your credit score as a key factor in your second loan approval. In addition to the appraisal, you may have to pay additional fees, such as survey fees, attorney fees, and fees for flood and natural hazard disclosure reports. You may also need to purchase title insurance.

Get an appraisal

A home equity loan, also known as HELOC, can be a loan that you can get based upon the equity in your home. This type of loan allows you to borrow the maximum amount within a specified period of time. For you to be eligible, your credit score must be at least 620 and you must have a low debt/income ratio. A home appraisal is vital because it informs the lender how much you owe. An appraisal isn't necessary. An appraisal does not have to be done. Financial intuition can help you determine the amount of equity in your portfolio.

The appraiser will inspect the inside and outside of your home and gather information on its features. The appraiser will inspect the home from all angles and also compare it with other similar properties in your area. They will also examine any exterior improvements.

Reverse mortgage and heloc: Getting a Heloc

Reverse mortgages require you to meet certain requirements. These qualifications include a detailed appraisal of the property. A line of credit is an option if the property is valued less than its appraisal. But, you will need to make regular monthly payments. This could damage your credit and lead to foreclosure. Reverse mortgages, on the other hand, do not require monthly payments but are less costly to set up. You will need to live in your property and pay all taxes and insurance on the due date.

One of the most important considerations when applying for a reverse mortgage is your ability to repay it. HELOCs as well reverse mortgages are both based on the ability to repay method. This calculates a borrower’s debt-to-income ratio. It is much easier to get the reverse mortgage if you have a fixed income.

FAQ

What is a reverse mortgage?

A reverse mortgage lets you borrow money directly from your home. It works by allowing you to draw down funds from your home equity while still living there. There are two types of reverse mortgages: the government-insured FHA and the conventional. A conventional reverse mortgage requires that you repay the entire amount borrowed, plus an origination fee. FHA insurance covers your repayments.

How can I find out if my house sells for a fair price?

Your home may not be priced correctly if your asking price is too low. A home that is priced well below its market value may not attract enough buyers. Our free Home Value Report will provide you with information about current market conditions.

Can I buy a house in my own money?

Yes! Yes. These programs include government-backed mortgages (FHA), VA loans and USDA loans. You can find more information on our website.

What should I be looking for in a mortgage agent?

A mortgage broker assists people who aren’t eligible for traditional mortgages. They compare deals from different lenders in order to find the best deal for their clients. Some brokers charge a fee for this service. Others offer no cost services.

Statistics

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

External Links

How To

How to Manage a Rental Property

It can be a great way for you to make extra income, but there are many things to consider before you rent your house. We'll help you understand what to look for when renting out your home.

Here are some things you should know if you're thinking of renting your house.

-

What is the first thing I should do? Before you decide if your house should be rented out, you need to examine your finances. You may not be financially able to rent out your house to someone else if you have credit card debts or mortgage payments. You should also check your budget - if you don't have enough money to cover your monthly expenses (rent, utilities, insurance, etc. It may not be worth it.

-

What is the cost of renting my house? Many factors go into calculating the amount you could charge for letting your home. These include factors such as location, size, condition, and season. Keep in mind that prices will vary depending upon where you live. So don't expect to find the same price everywhere. Rightmove estimates that the market average for renting a 1-bedroom flat in London costs around PS1,400 per monthly. This means that if you rent out your entire home, you'd earn around PS2,800 a year. This is a good amount, but you might make significantly less if you let only a portion of your home.

-

Is it worth the risk? There are always risks when you do something new. However, it can bring in additional income. Make sure that you fully understand the terms of any contract before you sign it. Your home will be your own private sanctuary. However, renting your home means you won't have to spend as much time with your family. Before signing up, be sure to carefully consider these factors.

-

Are there any advantages? Now that you have an idea of the cost to rent your home, and are confident it is worth it, it is time to consider the benefits. There are many reasons to rent your home. You can use it to pay off debt, buy a holiday, save for a rainy-day, or simply to have a break. It is more relaxing than working every hour of the day. If you plan ahead, rent could be your full-time job.

-

How can I find tenants Once you decide that you want to rent out your property, it is important to properly market it. Listing your property online through websites like Rightmove or Zoopla is a good place to start. Once potential tenants contact you, you'll need to arrange an interview. This will help you assess their suitability and ensure they're financially stable enough to move into your home.

-

What can I do to make sure my home is protected? If you're worried about leaving your home empty, you'll need to ensure you're fully protected against damage, theft, or fire. You will need insurance for your home. This can be done through your landlord directly or with an agent. Your landlord will likely require you to add them on as additional insured. This is to ensure that your property is covered for any damages you cause. If your landlord is not registered with UK insurers, or you are living abroad, this policy doesn't apply. In such cases, you will need to register for an international insurance company.

-

Sometimes it can feel as though you don’t have the money to spend all day looking at tenants, especially if there are no other jobs. But it's crucial that you put your best foot forward when advertising your property. Post ads online and create a professional-looking site. You'll also need to prepare a thorough application form and provide references. Some prefer to do it all themselves. Others hire agents to help with the paperwork. It doesn't matter what you do, you will need to be ready for questions during interviews.

-

What happens after I find my tenant?After you've found a suitable tenant, you'll need to agree on terms. If there is a lease, you will need to inform the tenant about any changes such as moving dates. If this is not possible, you may negotiate the length of your stay, deposit, as well as other details. While you might get paid when the tenancy is over, utilities are still a cost that must be paid.

-

How do I collect rent? You will need to verify that your tenant has actually paid the rent when it comes time to collect it. If not, you'll need to remind them of their obligations. After sending them a final statement, you can deduct any outstanding rent payments. If you're struggling to get hold of your tenant, you can always call the police. The police won't ordinarily evict unless there's been breach of contract. If necessary, they may issue a warrant.

-

What can I do to avoid problems? It can be very lucrative to rent out your home, but it is important to protect yourself. Install smoke alarms, carbon monoxide detectors, and security cameras. You should also check that your neighbors' permissions allow you to leave your property unlocked at night and that you have adequate insurance. You must also make sure that strangers are not allowed to enter your house, even when they claim they're moving in the next door.