A Home equity line credit (HELOC), or a credit card linked to your equity in your house, is a credit option. This is a great option for elderly homeowners, and it can be used to consolidate your debt. It does have some drawbacks. Here are the pros and cons of this credit card.

Credit line for home equity

Home equity lines can be secured by equity in your home. They can be a valuable financial tool for homeowners. The lender will allow you to borrow as much as 60% or as much 85% of your equity. These loans offer flexibility and lower interest rates but they also have some drawbacks.

A home equity credit line of credit can be a viable financial option. However, there are pros and cons to consider. You will be required to pay interest on the entire loan amount. You may also be charged an inactivity charge by some lenders if the funds aren't used within a given time.

It is a credit card that you can link to the equity in your home.

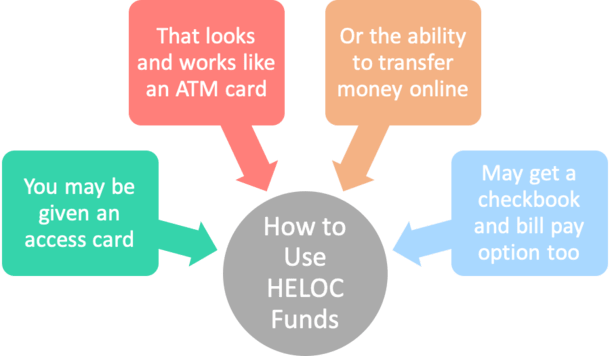

HELOCs can be revolving lines of credit similar to credit cards, but linked to the equity in your house. It can be used to make large purchases or pay off higher-interest debt. You can borrow however much you wish, but only up to what you have. This type of credit usually has a lower interest rate than other loans and may even be tax-deductible.

The HELOC can also be used to pay for major purchases, or for a vacation. It can be used to reduce high-interest debt or pay for a new vehicle, as well as for unexpected expenses. You should remember that your credit line is tied directly to your equity in your home and should not be used for large purchases. Lenders will evaluate your ability to repay the credit line as well as other financial obligations.

It's an attractive option for older homeowners

A HELOC is an unsecured line of credit that can be repaid over time. This allows seniors to borrow money without having to make a down payment. These loans are secured by the homeowner's equity. If you are unable or unwilling to make the payments, the lender has the right to repossess the property. In addition, a HELOC can be used to finance educational expenses for children or grandchildren. It can be used to fund home improvements and medical bills.

Another advantage of HELOCs is their low interest rates. HELOCs are significantly cheaper than reverse mortgages, and they offer greater flexibility. But they have their disadvantages.

It can be used to consolidate debt

A HELOC is an excellent way to consolidate your debts and simplify your finances. A HELOC can be combined with all your debt to reduce interest. A HELOC typically comes with lower interest rates than a credit card or a secured personal loan. Citizens provides two repayment options and support throughout the entire process. You can use your equity to repay your high-interest debt.

A HELOC can be used to pay off high-interest credit card debts. It has a longer draw period than a credit card, so you can be more flexible with your payments. The principle balance of your HELOC can be paid in additional payments, which will reduce your interest payments. One advantage to using a HELOC for consolidating debt is its ability to improve your credit score.

It can also be used to purchase a new home.

HELOCs can only be used to purchase a second house. You pay no interest for the amount you use. The flexibility of HELOCs makes them very attractive. The equity in your home can be used to reduce your debt. Income from an investment property can also be used to offset your debt. If you have sufficient income to cover the mortgage payments, you may be eligible to buy the second home with the income that you get from it. However, you should be aware that you will be exposed to changes in the housing market.

You may need additional capital to cover the down payment or other expenses if you are looking to purchase a second house. A HELOC can be taken against equity in your home. However, you will not be able to take out a HELOC if your current home is still on the market.

FAQ

What time does it take to get my home sold?

It all depends upon many factors. These include the condition of the home, whether there are any similar homes on the market, the general demand for homes in the area, and the conditions of the local housing markets. It may take up to 7 days, 90 days or more depending upon these factors.

How long does it take to get a mortgage approved?

It all depends on your credit score, income level, and type of loan. It takes approximately 30 days to get a mortgage approved.

How many times do I have to refinance my loan?

It all depends on whether your mortgage broker or another lender is involved in the refinance. Refinances are usually allowed once every five years in both cases.

What should I look for when choosing a mortgage broker

Mortgage brokers help people who may not be eligible for traditional mortgages. They compare deals from different lenders in order to find the best deal for their clients. This service may be charged by some brokers. Other brokers offer no-cost services.

Can I buy a house in my own money?

Yes! There are programs available that allow people who don't have large amounts of cash to purchase a home. These programs include government-backed mortgages (FHA), VA loans and USDA loans. Visit our website for more information.

How can I eliminate termites & other insects?

Termites and other pests will eat away at your home over time. They can cause serious damage and destruction to wood structures, like furniture or decks. It is important to have your home inspected by a professional pest control firm to prevent this.

Statistics

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

External Links

How To

How to locate an apartment

The first step in moving to a new location is to find an apartment. This takes planning and research. This involves researching and planning for the best neighborhood. This can be done in many ways, but some are more straightforward than others. Before you rent an apartment, consider these steps.

-

Researching neighborhoods involves gathering data online and offline. Websites such as Yelp. Zillow. Trulia.com and Realtor.com are some examples of online resources. Local newspapers, real estate agents and landlords are all offline sources.

-

Find out what other people think about the area. Yelp and TripAdvisor review houses. Amazon and Amazon also have detailed reviews. You can also check out the local library and read articles in local newspapers.

-

Call the local residents to find out more about the area. Talk to those who have lived there. Ask them about their experiences with the area. Ask for recommendations of good places to stay.

-

Check out the rent prices for the areas that interest you. If you are concerned about how much you will spend on food, you might want to rent somewhere cheaper. However, if you intend to spend a lot of money on entertainment then it might be worth considering living in a more costly location.

-

Find out all you need to know about the apartment complex where you want to live. It's size, for example. What is the cost of it? Is it pet-friendly What amenities does it have? Are there parking restrictions? Are there any rules for tenants?