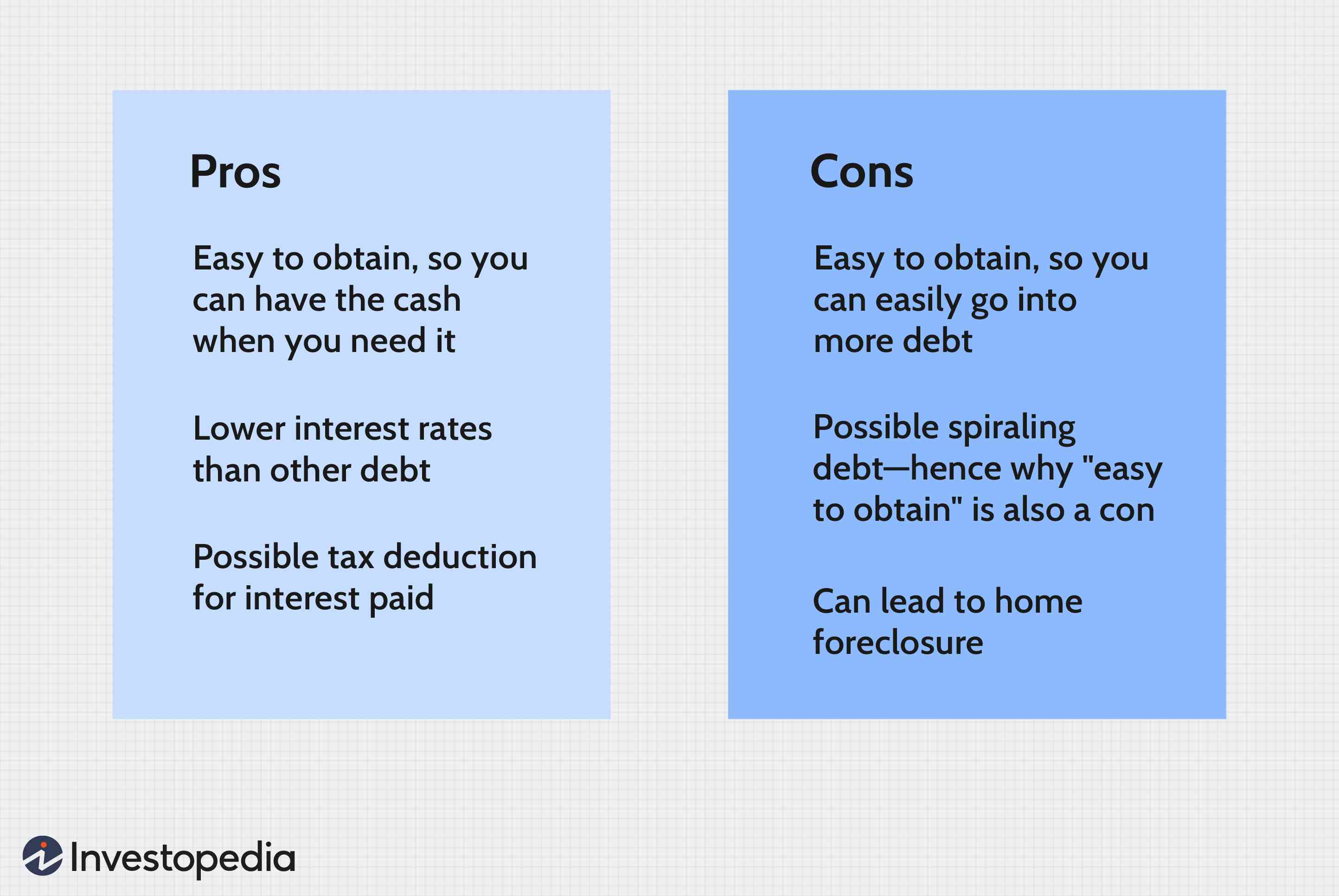

A refinance allows you to borrow money against the equity of your home. Home equity loans are an option for those who require additional funds but don't have enough cash. Although both options are viable, cash-out refinances can be smart for homeowners with equity in the home. While cash-out refinances have lower interest rates and are generally easier to get, they can be more expensive.

Cash-out refinances offer lower interest rates

A cash-out mortgage can allow you to tap into the equity in your house without having to borrow as much. You should also consider the potential drawbacks to this loan. Depending on your situation, a cash-out refinance can increase the debt you have on your mortgage, increase your payment period, or even put you at risk of foreclosure if you do not pay your loan.

While cash-out refinances usually have lower interest rates that home equity loans, you will still need to pay fees. Closing fees can amount to up to 3 percent of the new mortgage. Property taxes and homeowners insurance are also required. However, if your credit score has improved, cash-out mortgage refinances could be a good choice.

They are easier to qualify for

A home equity loan allows homeowners to borrow against their equity. These loans usually have lower interest rates than home mortgage refinances and are therefore easier to qualify for. A home equity loan might also have a lower closing fee and be more flexible then a traditional mortgage. It is important that you understand the requirements before applying for a home equity mortgage.

A home equity loan lets you borrow against the equity in your house and then repay it in an agreed amount of installments that includes interest and any fees. The loan is also known as a "second mortgage" as it is secured against your home. This means that the lender could foreclose on you home if your loan defaults. Although refinancing may be more accessible than a home equity mortgage, it is still important to take into account all aspects before you make a decision.

They are more convenient

If you have good credit and a large amount of equity in your home, a home equity loan might be a good option. A cash-out refinance may be a better option if you need to reduce your monthly mortgage payments. It is worth getting quotes from multiple lenders before making your final decision. A detailed list of fees for lending should be requested.

Refinances are loans that replace your existing mortgage. A home equity loan is a loan that you take out over your existing mortgage. Both products have advantages and disadvantages. Before you decide which one is best for your needs, it is important that you fully understand the risks associated with each.

They are more expensive

A refinance loan will save you money long term because you can access the equity in your house. The refinance loan will cost you more upfront than a home equity loan but your monthly payments are lower. A home equity loan will still be affordable if your goal is to repay the loan in six or less months.

It is easier to get a home equity loan. It will require you to pay closing fees. These costs are generally not tax-deductible. A home equity loan has another advantage: flexibility. You can use the money for major purchases, or to pay off other large expenses.

FAQ

How long does it take to get a mortgage approved?

It depends on several factors including credit score, income and type of loan. It typically takes 30 days for a mortgage to be approved.

How much does it cost for windows to be replaced?

Window replacement costs range from $1,500 to $3,000 per window. The cost of replacing all your windows will vary depending upon the size, style and manufacturer of windows.

Which is better, to rent or buy?

Renting is generally cheaper than buying a home. It is important to realize that renting is generally cheaper than buying a home. You will still need to pay utilities, repairs, and maintenance. The benefits of buying a house are not only obvious but also numerous. For instance, you will have more control over your living situation.

Can I afford a downpayment to buy a house?

Yes! Yes. There are programs that will allow those with small cash reserves to purchase a home. These programs include FHA, VA loans or USDA loans as well conventional mortgages. More information is available on our website.

What should I consider when investing my money in real estate

The first step is to make sure you have enough money to buy real estate. If you don’t save enough money, you will have to borrow money at a bank. It is important to avoid getting into debt as you may not be able pay the loan back if you default.

You also need to make sure that you know how much you can spend on an investment property each month. This amount must be sufficient to cover all expenses, including mortgage payments and insurance.

It is important to ensure safety in the area you are looking at purchasing an investment property. You would be better off if you moved to another area while looking at properties.

Statistics

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

External Links

How To

How to Rent a House

For people looking to move, finding houses to rent is a common task. But finding the right house can take some time. Many factors affect your decision-making process when choosing a home. These factors include size, amenities, price range, location and many others.

It is important to start searching for properties early in order to get the best deal. Also, ask your friends, family, landlords, real-estate agents, and property mangers for recommendations. This will give you a lot of options.