You should be familiar with the basics of a mortgage before you apply. These include the interest rate, down payment, as well as Lender's assessment. The first step to buying a house is choosing the right mortgage. It can make a huge difference in the quality of your life and in your finances.

Interest rate

A percentage of the loan amount is used to calculate the interest rate for a mortgage. The borrower pays this amount on top of the agreed loan repayments. Choosing the right mortgage interest rate is crucial for a person to be able to make their monthly payments. Mortgage interest rates can rise and fall so it is important that you keep an eye on them.

The interest rate does not include other costs that may be associated with the mortgage, such as loan origination fees and discount points. Mortgage insurance and closing costs are also included. Borrowers will be able to see the total cost of borrowing by using the APR.

Down payment

A down payment is a portion of the total home's value that the borrower makes up front. It can range from 10 to 50 percent. The interest rate that will be charged to a mortgage borrower will depend on the amount of their down payment. The interest rate will be lower if the downpayment is higher. A large down payment reduces the risk of banks lending mortgages.

While there are no hard and fast rules as to how much down payment you need, there are some factors you should consider when determining your down payment. Low down payments are risky. It's best to aim for at most fifty percent. A bank is more likely to lend money to borrowers who can put up fifty to sixty percent of the purchase price. However, if your down payment is small or you don't have any savings, a bank will likely refuse to lend you money if you can't pay the full amount in a lump sum.

Lender's assessment on your information

A mortgage lender examines many factors to determine if your risk level. They will examine your credit history and any recent debt applications. They may contact your employer to verify these details. They may also check your payment history to determine if you have been punctual with your payments or if there have been late payments. And, if you have any substantial assets, they'll look at them as well.

Lenders are interested in knowing if you can repay the loan. They may also be interested in your creditworthiness as well as your ability to pay off more debt. They use the five Cs of credit to determine creditworthiness: capacity, character, capital, collateral, conditions, and conditions.

Types of mortgages

There are several different types of mortgages. Conventional mortgages are the first type. A conventional mortgage can be used for most types of property. These loans are backed generally by the government and are easier to qualify for. These mortgages are better for people who are first-time home buyers or have lower credit scores.

The adjustable-rate mortgage (ARM) is the second type. If you like to make adjustments to your interest rates, adjustable rate mortgages are the best choice. Another type of loan is a government-backed one, such an FHA, VA or USDA mortgage.

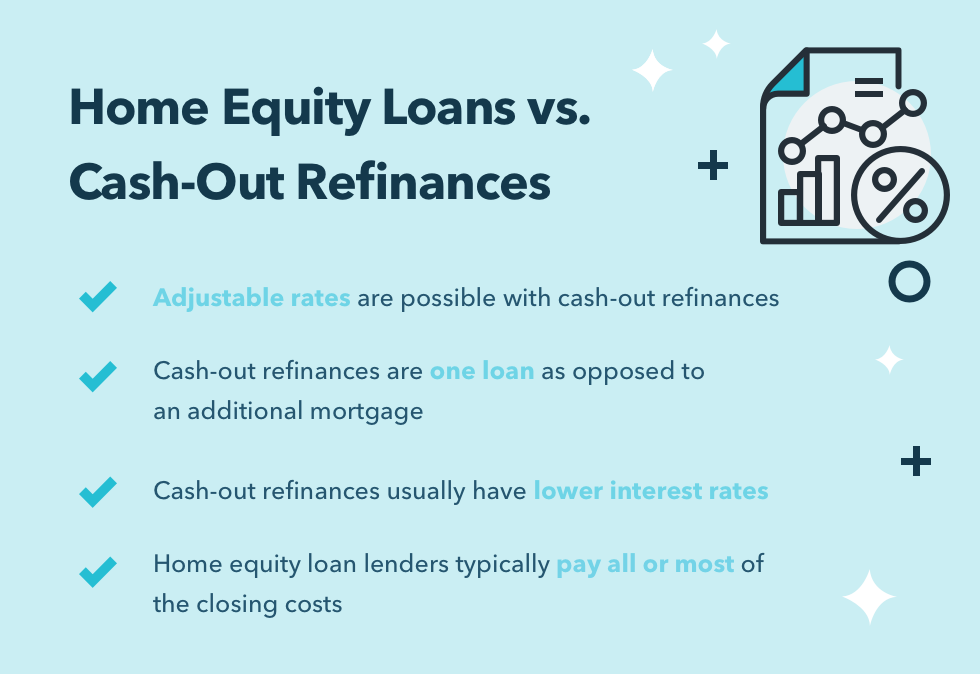

Refinancing options

There are many options available if you're looking to refinance your mortgage. You should shop around to find the best deal. Before you refinance, it is important to get quotes from multiple lenders. You can also use an attorney to help you navigate the complicated paperwork.

Refinancing allows you to take advantage of the equity in your home. Refinancing will lower your monthly cost and make it possible to achieve your financial goals. Most people choose to refinance their mortgages for various reasons, including lower interest rates, shortening their payment terms, and cashing out their home equity.

FAQ

Can I get another mortgage?

Yes. But it's wise to talk to a professional before making a decision about whether or not you want one. A second mortgage is usually used to consolidate existing debts and to finance home improvements.

What are the advantages of a fixed rate mortgage?

Fixed-rate mortgages guarantee that the interest rate will remain the same for the duration of the loan. This means that you won't have to worry about rising rates. Fixed-rate loans also come with lower payments because they're locked in for a set term.

What's the time frame to get a loan approved?

It depends on several factors such as credit score, income level, type of loan, etc. It usually takes between 30 and 60 days to get approved for a mortgage.

How can I tell if my house has value?

Your home may not be priced correctly if your asking price is too low. Your asking price should be well below the market value to ensure that there is enough interest in your property. Our free Home Value Report will provide you with information about current market conditions.

How much does it cost to replace windows?

Replacement windows can cost anywhere from $1,500 to $3,000. The exact size, style, brand, and cost of all windows replacement will vary depending on what you choose.

Are flood insurance necessary?

Flood Insurance covers flooding-related damages. Flood insurance helps protect your belongings, and your mortgage payments. Find out more information on flood insurance.

Statistics

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

External Links

How To

How to find real estate agents

Agents play an important role in the real-estate market. They can sell properties and homes as well as provide property management and legal advice. A good real estate agent should have extensive knowledge in their field and excellent communication skills. Look online reviews to find qualified professionals and ask family members for recommendations. It may also make sense to hire a local realtor that specializes in your particular needs.

Realtors work with homeowners and property sellers. A realtor's job it to help clients purchase or sell their homes. Apart from helping clients find the perfect house to call their own, realtors help manage inspections, negotiate contracts and coordinate closing costs. Most realtors charge a commission fee based on the sale price of the property. Unless the transaction closes, however, some realtors charge no fee.

There are many types of realtors offered by the National Association of REALTORS (r) (NAR). NAR requires licensed realtors to pass a test. A course must be completed and a test taken to become certified realtors. NAR designates accredited realtors as professionals who meet specific standards.