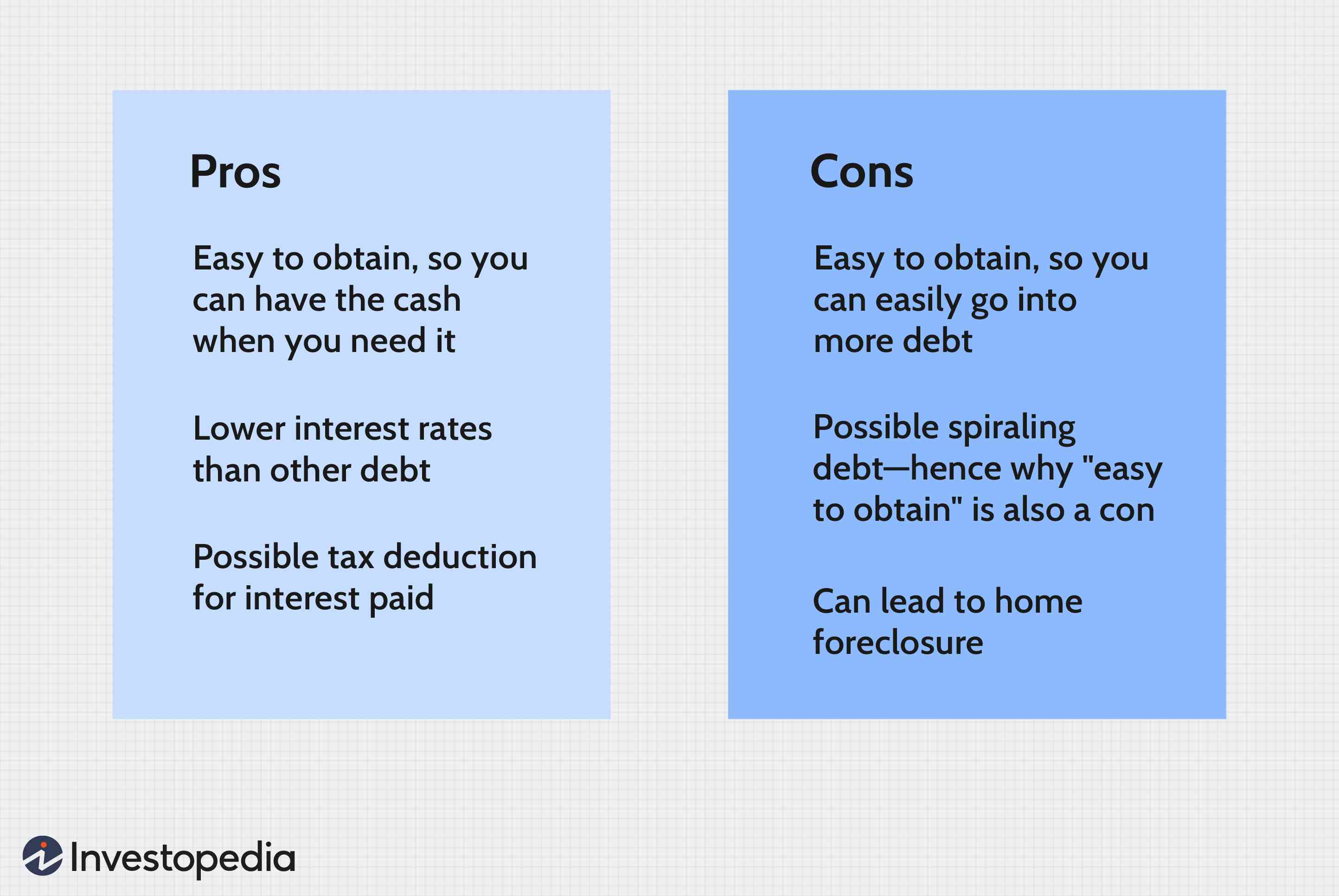

A mortgage rate lock can protect you against future rate increases. These types allow your lender and you to finalize your mortgage without worrying about a rate hike. Interest rate locks can be costly so make sure to evaluate whether locking your mortgage rate is worth the risk.

Interest rate locks protect your from interest rate rises

A interest rate lock can protect you from rising interest rates when you refinance your home or purchase a new one. This type protection is only available for a brief period and can be very helpful for home buyers. It is important that you carefully read the rate lock policy from your lender. Rate locks are not allowed by all lenders. Some lenders may even alter them at any time.

The good thing is that there are many methods to protect yourself against rising interest rates. A floating interest rate lock is another option. This lock will protect you from rising interest rates and allow you to save money when rates fall. This lock usually costs 0.5% to 1 percent of the loan amount up front.

These documents allow your lender finalize your loan

Mortgage rate locks protect you against rate jumps and market fluctuations. Locks will protect you from paying more than the current interest rate, and will also give you financial security when refinancing your loan. Rate locks are typically available for 30 days, although some lenders will offer longer rates.

It is expensive to lock in a mortgage interest rate. To close your loan, lenders will charge a fee. In most cases, the fee for locking your loan is included in total loan amount. It may be worth it to pay the small fee if it means keeping your monthly payments down.

They could be subject to additional charges

Be sure to review the terms before locking your mortgage rate. Terms can vary between providers. You may find that your rate lock provider can change the margin or prepayment penalty, indexes and caps at any point. You may also lock your rate and later find that it has increased in significant ways. This can lead you to having a major headache. It's possible to lock your rate and then find out later that it has increased significantly.

A written commitment is usually required from the lender to lock mortgage rates. The lender must disclose to the borrower the interest rate, discount and other charges. You must also provide written notice to your lender within three business days of locking your interest rate. The state in which you reside may require you to sign a formal Lock-In Agreement. This document should list all applicable fees and expenses and should be included in your Loan Estimate.

When to lock in a mortgage rate

Before you decide on the type or loan you want to take, it is important that your mortgage rate be locked in. This is a binding contract between you and the lender. The lock will continue in effect until the closing date. If you change your credit score or application while you are locked in, your interest rate will change, and you will not be eligible for the same loan interest rate.

You should monitor mortgage rates frequently as they fluctuate. The mortgage lender must notify the borrower if the rates go down. You can also add a "float down" provision to your lock. However, this will cost you a bit more. Make sure you know the time frame for locking in your mortgage rate.

FAQ

Can I buy a house without having a down payment?

Yes! Yes! There are many programs that make it possible for people with low incomes to buy a house. These programs include FHA, VA loans or USDA loans as well conventional mortgages. More information is available on our website.

What are the 3 most important considerations when buying a property?

Location, price and size are the three most important aspects to consider when purchasing any type of home. Location is the location you choose to live. Price refers how much you're willing or able to pay to purchase the property. Size refers how much space you require.

Is it better buy or rent?

Renting is often cheaper than buying property. However, you should understand that rent is more affordable than buying a house. The benefits of buying a house are not only obvious but also numerous. You'll have greater control over your living environment.

How much does it take to replace windows?

Replacing windows costs between $1,500-$3,000 per window. The total cost of replacing all of your windows will depend on the exact size, style, and brand of windows you choose.

Statistics

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

External Links

How To

How do I find an apartment?

Finding an apartment is the first step when moving into a new city. This involves planning and research. This includes researching the neighborhood, reviewing reviews, and making phone call. Although there are many ways to do it, some are easier than others. Before you rent an apartment, consider these steps.

-

Online and offline data are both required for researching neighborhoods. Websites such as Yelp. Zillow. Trulia.com and Realtor.com are some examples of online resources. Online sources include local newspapers and real estate agents as well as landlords and friends.

-

See reviews about the place you are interested in moving to. Yelp. TripAdvisor. Amazon.com have detailed reviews about houses and apartments. You might also be able to read local newspaper articles or visit your local library.

-

You can make phone calls to obtain more information and speak to residents who have lived there. Ask them what the best and worst things about the area. Ask them if they have any recommendations on good places to live.

-

Check out the rent prices for the areas that interest you. Renting somewhere less expensive is a good option if you expect to spend most of your money eating out. Consider moving to a higher-end location if you expect to spend a lot money on entertainment.

-

Find out about the apartment complex you'd like to move in. What size is it? What price is it? Is it pet friendly? What amenities is it equipped with? Do you need parking, or can you park nearby? Do tenants have to follow any rules?