Paying PMI upfront is an option if your intention is to live in the house for many years. The upfront premium can be used for your downpayment or home equity. You may also be able to refinance the loan to avoid paying monthly insurance. You should consider the associated costs before you even consider this option. It can have a significant effect on your monthly mortgage payments. So make sure to weigh all your options before you commit.

Alternatives to paying PMI upfront

There are several ways to save on your mortgage. Refinancing your mortgage or purchasing the insurance yourself can help you avoid PMI. Be aware, however, that these options are subject to restrictions. Additionally, you may have to pay a higher interest rate. These options are not as effective at eliminating PMI as the old type.

While some people may dislike the PMI concept, it makes the most sense when compared to other loan options. You could save hundreds of thousands by asking your lender for a PMI Loan. Here are some of these options: One of the best ways to avoid paying PMI is to have a larger down payment. You'll be able negotiate a lower selling price with the seller if you have more money to deposit.

A monthly premium plan is also an option. This plan is ideal for those who have extra income or wish to keep their housing costs down. The monthly premium will depend on the loan amount. You can also choose to pay a single premium upfront.

Calculating your PMI payment

You will need to consider your credit score, loan-to-value ratio and other factors when determining your PMI payment. These factors will give you an idea of the monthly payment. You should also consider how much you plan to put down as a down payment. In certain cases, a small down payment could reduce your PMI cost significantly.

Depending on the type of mortgage you have, PMI can be paid as a one-time payment or a monthly premium. The latter is more common as it requires no upfront payment. You should know that the monthly payment will likely be higher as a result.

PMI is an extra expense but can bring significant benefits to your long term wealth building. It allows you to buy a home quicker and builds equity. However, it's important to keep in mind that you'll need to pay at least as much PMI as the price of the home itself.

Refinance your mortgage to eliminate PMI

Private mortgage insurance (PMI), is required for conventional loans that require less then 20% down. If your loan balance is higher than 80%, you may be able to remove PMI by refinancing your loan. This method can lower your monthly payments while allowing you to keep as much equity as possible in your home.

PMI is an expense that can increase your monthly payment by hundreds of dollars. To remove PMI from your loan, refinance can be a good option to get rid of it and reduce your monthly payment. Some homeowners are able to refinance into a loan without PMI, while others must refinance into a different loan. Before you begin the process, it's important to be aware of the requirements.

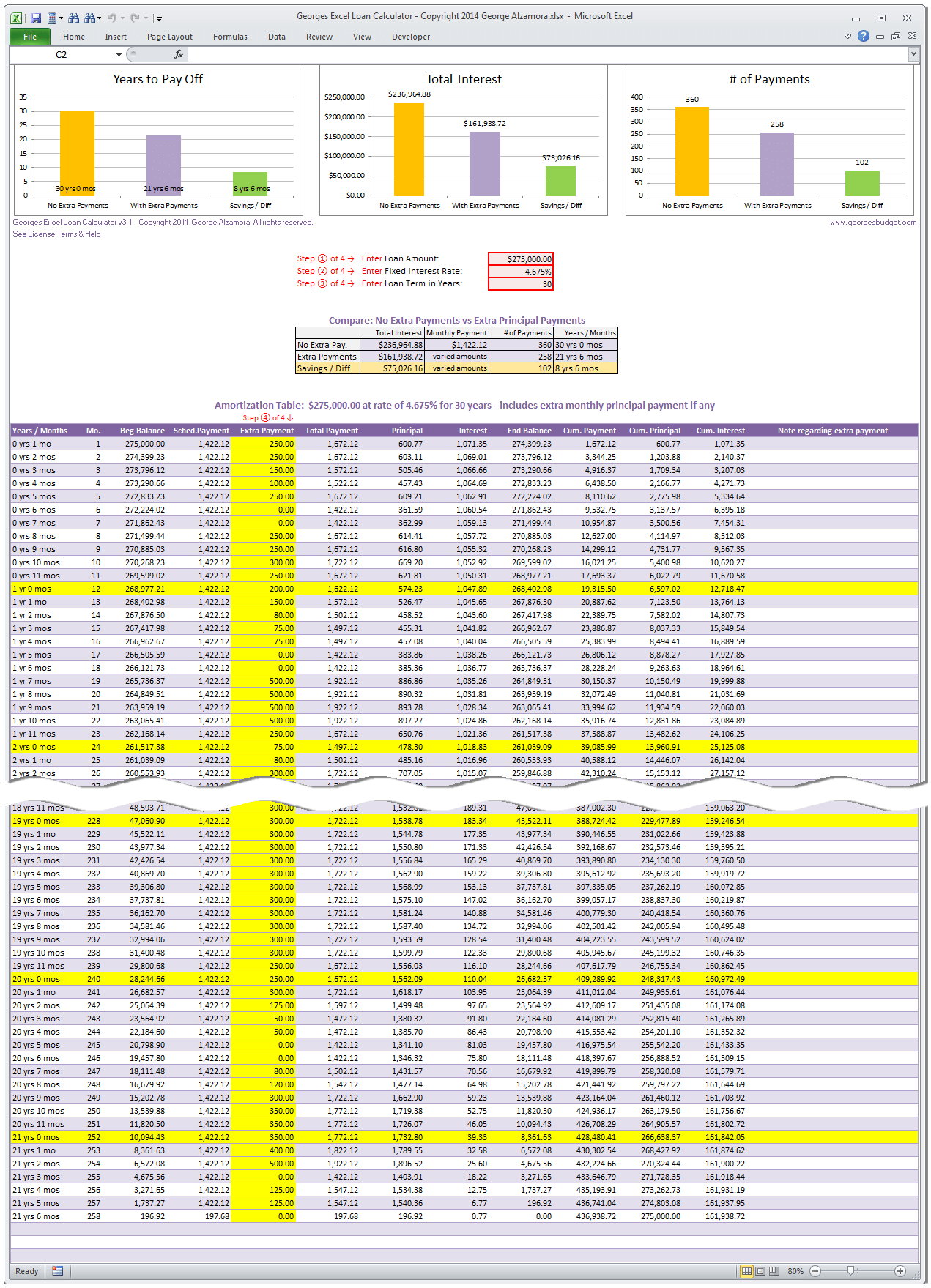

There are a few factors you should keep in mind when refinancing your loan to remove PMI. First, you need to know how much money it would cost you to save your loan and how much you'd have to pay back if the loan wasn't refinanced. A refinance calculator will help you calculate how much money you could save by refinancing your loan.

FAQ

How can I eliminate termites & other insects?

Your home will eventually be destroyed by termites or other pests. They can cause severe damage to wooden structures, such as decks and furniture. This can be prevented by having a professional pest controller inspect your home.

What are the chances of me getting a second mortgage.

Yes. But it's wise to talk to a professional before making a decision about whether or not you want one. A second mortgage is usually used to consolidate existing debts and to finance home improvements.

How much money can I get to buy my house?

The number of days your home has been on market and its condition can have an impact on how much it sells. According to Zillow.com, the average home selling price in the US is $203,000 This

Which is better, to rent or buy?

Renting is usually cheaper than buying a house. But, it's important to understand that you'll have to pay for additional expenses like utilities, repairs, and maintenance. There are many benefits to buying a home. You will have greater control of your living arrangements.

What should I do if I want to use a mortgage broker

If you are looking for a competitive rate, consider using a mortgage broker. Brokers are able to work with multiple lenders and help you negotiate the best rate. Brokers may receive commissions from lenders. Before you sign up, be sure to review all fees associated.

Statistics

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

External Links

How To

How to find houses to rent

Renting houses is one of the most popular tasks for anyone who wants to move. It can be difficult to find the right home. When choosing a house, there are many factors that will influence your decision making process. These include location, size, number of rooms, amenities, price range, etc.

We recommend you begin looking for properties as soon as possible to ensure you get the best deal. Consider asking family, friends, landlords, agents and property managers for their recommendations. This will give you a lot of options.