Before applying for a HELOC, consider the pros and cons of this type of credit. HELOCs come with no closing costs. However the interest on funds you use for personal purposes is not tax deductible. However, you could overspend on your HELOC, taping out equity and then facing high interest and principal payments. The good news about this is that interest rates are less than on traditional 30-year fixed-rate home Equity loans.

The interest charged on funds received from a HELOC that are used to pay personal expenses is no longer tax deductible

You might be curious if interest on your HELOC still qualifies for tax deduction. There are still $750,000 worth of interest payments that can be deducted from a HELOC. The interest you pay on funds for personal expenses like home repairs, however, will not be allowable. This is due to the fact that the new tax law changes the way you can deduct interest payments from personal expenses.

In the past, homeowners could claim interest up to $100,000 from a HELOC. However, homeowners can now only deduct home improvements that increase the home's market value under the new tax law. However, these improvements must be substantial and must increase its market value. A substantial improvement refers to an improvement that significantly raises the value of the house, such as a new kitchen and extension.

The tax code mandates that any interest charged on a home equity loan must be used for collateral. This rule doesn't apply to personal expenses.

No closing costs to set up a HELOC

While no closing costs can be a benefit to a HELOC loan, it is important that you consider all costs before making a decision. Closing costs may be charged by the lender in addition to the interest rate. Before making a decision, you should shop around for lower costs. The average closing cost is between 2% and 5% of the total line.

HELOC is an revolving line credit that uses your equity as collateral. These funds can be used for various purposes including home renovations and medical expenses. The equity in the home is used to determine the credit limit. The "draw period", which is usually ten years, is also used by lenders. Borrowers must repay the loan within ten years. Borrowers might be able to extend the loan if necessary.

HELOC lenders can charge closing costs. However, these fees are typically much less than other costs. You may need to pay an application fee and an origination fee. These fees will ensure that the loan is legally binding without any liens. An appraisal or credit report may also be requested by the lender.

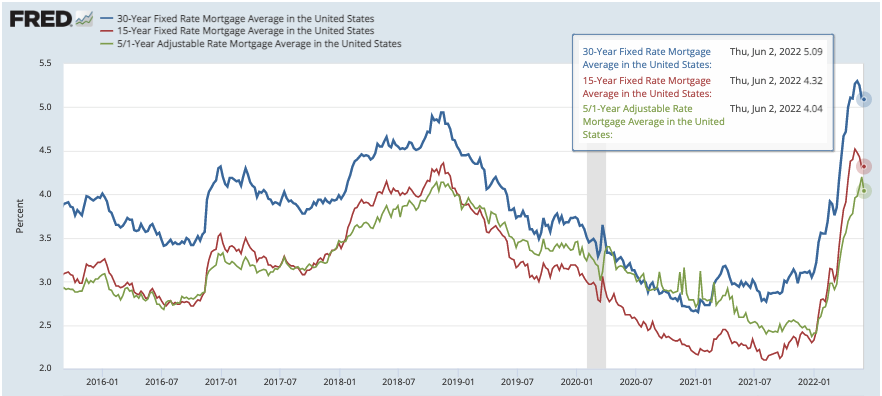

Higher interest rates than a 30-year fixed home equity loan

A home equity loan is a loan secured against the home's equity. The loan is paid in lump-sums and then interest-free over a predetermined period. A home equity line-of credit (HELOC), on the other hand, functions as a credit card but you pay only interest on the amount borrowed, and not the entire amount.

A home equity loan has a fixed-rate rate and a repayment period between 5 and 30 years. You will be able to lock in your interest rates regardless of economic conditions. Fixed-rate home equity loans often have lower interest rates that other types of loans. In some cases, as low as 3.3%.

Home equity lines of credit allow borrowers to access funds as needed. They are an excellent option if your goal is to complete a home improvement project, or repay existing debt. Home equity lines of credit have lower interest rates than other loans, but you will need a high credit score and a low debt-to-income ratio to qualify.

FAQ

What is the average time it takes to sell my house?

It all depends upon many factors. These include the condition of the home, whether there are any similar homes on the market, the general demand for homes in the area, and the conditions of the local housing markets. It takes anywhere from 7 days to 90 days or longer, depending on these factors.

What should you consider when investing in real estate?

The first thing to do is ensure you have enough money to invest in real estate. You will need to borrow money from a bank if you don’t have enough cash. It is also important to ensure that you do not get into debt. You may find yourself in defaulting on your loan.

It is also important to know how much money you can afford each month for an investment property. This amount must cover all expenses related to owning the property, including mortgage payments, taxes, insurance, and maintenance costs.

You must also ensure that your investment property is secure. It would be best to look at properties while you are away.

Can I buy a house without having a down payment?

Yes! There are many programs that can help people who don’t have a lot of money to purchase a property. These programs include government-backed loans (FHA), VA loans, USDA loans, and conventional mortgages. Visit our website for more information.

How much money will I get for my home?

This can vary greatly depending on many factors like the condition of your house and how long it's been on the market. Zillow.com reports that the average selling price of a US home is $203,000. This

Statistics

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

External Links

How To

How to buy a mobile home

Mobile homes are houses built on wheels and towed behind one or more vehicles. Mobile homes have been around since World War II when soldiers who lost their homes in wartime used them. Today, mobile homes are also used by people who want to live out of town. These houses come in many sizes and styles. Some houses are small, others can accommodate multiple families. Even some are small enough to be used for pets!

There are two types of mobile homes. The first type of mobile home is manufactured in factories. Workers then assemble it piece by piece. This takes place before the customer is delivered. You can also build your mobile home by yourself. The first thing you need to do is decide on the size of your mobile home and whether or not it should have plumbing, electricity, or a kitchen stove. Then, you'll need to ensure that you have all the materials needed to construct the house. To build your new home, you will need permits.

If you plan to purchase a mobile home, there are three things you should keep in mind. You might want to consider a larger floor area if you don't have access to a garage. A model with more living space might be a better choice if you intend to move into your new home right away. The trailer's condition is another important consideration. You could have problems down the road if you damage any parts of the frame.

Before buying a mobile home, you should know how much you can spend. It is important to compare prices across different models and manufacturers. It is important to inspect the condition of trailers. Although many dealerships offer financing options, interest rates will vary depending on the lender.

An alternative to buying a mobile residence is renting one. Renting allows the freedom to test drive one model before you commit. However, renting isn't cheap. Most renters pay around $300 per month.