The home equity line-of-credit works just like a primary credit. Before they can approve your loan, lenders want to know about the equity in your house, what it was appraised for, your income and credit score. This information is necessary to ensure that lenders are able to vet borrowers. They also want to know the value of the collateral, which is your home.

Getting a home equity line of credit

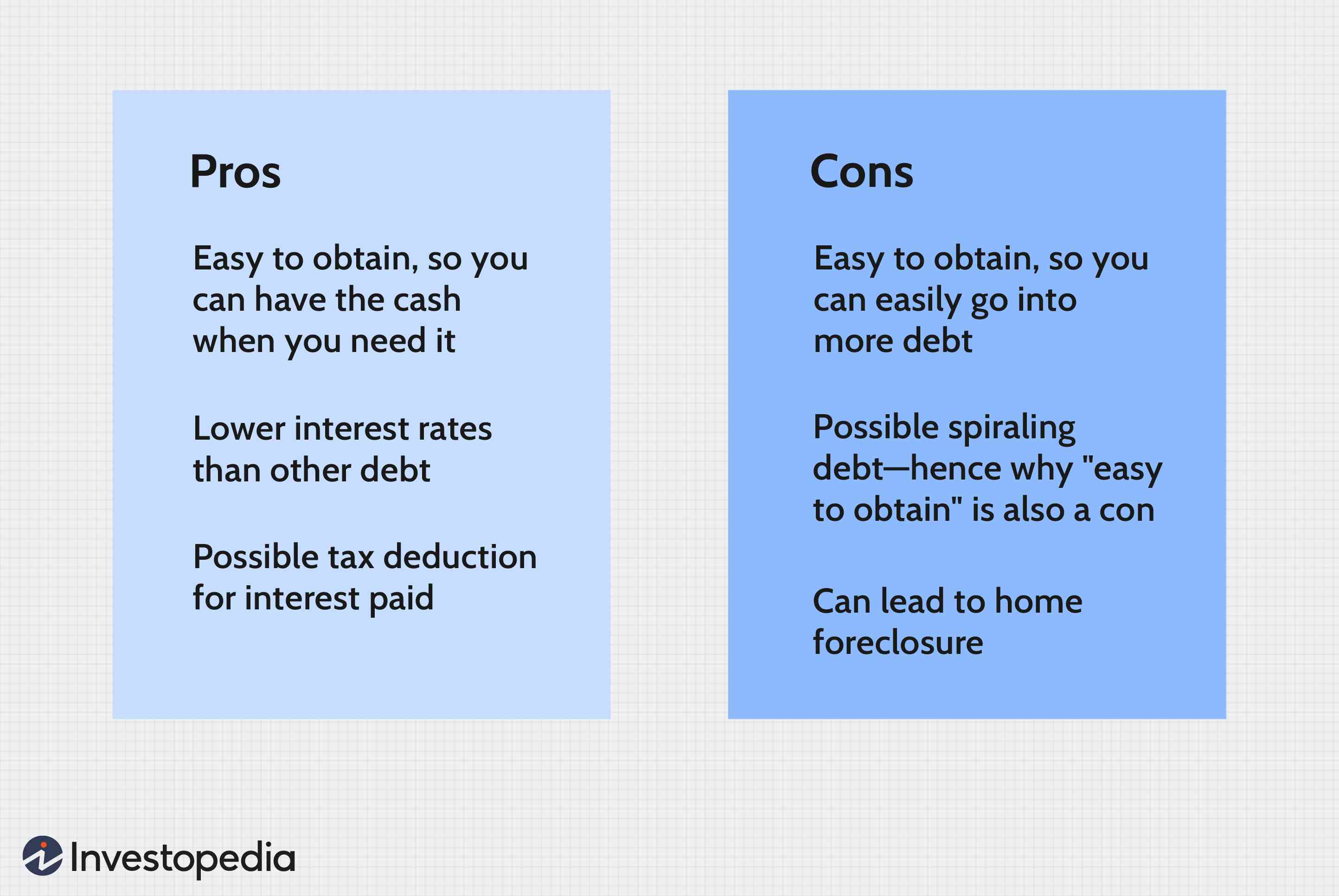

A home equity line of credit can be a good way to finance major expenses, such as home improvements or college tuition. Its prime rate is set by the Federal Reserve. The Federal Funds Interest Rate is generally 3% above the prime rate. The interest rate charged on home equity lines may be tax-deductible.

A home equity line of credit allows borrowers to access cash based on the value of their home, usually up to $50,000. The home equity line of credit works in the same way as a credit card but you only pay interest when you use it. Home equity lines also offer discounts depending on how much of your available credit is initially used.

To be eligible for a line of home equity credit, you must have a high credit score. While most lenders accept credit scores above 700, some will consider borrowers who have less credit. It is important to maintain your credit score high to obtain the best interest rates. You can also access more money with a home equity credit than you would get from a personal or credit card.

Repayment period

When determining the repayment term for a home equity credit line, there are many factors you should consider. First, make sure that you have enough equity in your home to qualify for the loan. You should also ensure that you are able to afford the higher monthly payments. This decision should be made keeping in mind your credit score and debt-to-income ratio.

A home equity line credit usually has a repayment term of 5-10 years. This period will see you make monthly payments, which include principal and any interest. This will allow you to pay down your debt quicker and lower your monthly payments. Depending on your individual situation, you might want to look into a payment plan that will help make your monthly payments more affordable.

HELOCs can be used to loan money based on the property's value and the remaining balance on your mortgage. It is a good idea to consult with your financial advisor to make sure you can afford the loan. Also, keep in mind that a HELOC may be unsuitable if you plan to sell the house.

Interest rate

A home equity line is a type loan secured by a homeowner’s home. The rate of interest is variable and can depend on several factors such as your creditworthiness and the loan to value ratio. To ensure the highest rate, there are some things you can do.

First, understand the terms of the loan. A home equity line of credit typically has two phases: a draw period and a repayment period. The draw period, which is typically around 10 year long, lasts for a fixed time. You'll make small interest only payments over this time. Any additional payments will go towards the principal.

A home equity line is a credit card that works similarly to a credit-card. However, you only pay interest for the amount you spend instead of the entire amount. The interest rate on a HELOC is typically lower than traditional mortgages or other types. Another benefit of a HELOC is that you don't need to repay the full amount at once.

FAQ

How much does it cost to replace windows?

The cost of replacing windows is between $1,500 and $3,000 per window. The cost of replacing all your windows will vary depending upon the size, style and manufacturer of windows.

How do I fix my roof

Roofs can leak because of wear and tear, poor maintenance, or weather problems. Minor repairs and replacements can be done by roofing contractors. For more information, please contact us.

Can I buy a house without having a down payment?

Yes! Yes! There are many programs that make it possible for people with low incomes to buy a house. These programs include FHA loans, VA loans. USDA loans and conventional mortgages. Visit our website for more information.

Is it possible sell a house quickly?

If you have plans to move quickly, it might be possible for your house to be sold quickly. There are some things to remember before you do this. First, find a buyer for your house and then negotiate a contract. Second, you need to prepare your house for sale. Third, it is important to market your property. You must also accept any offers that are made to you.

Should I use a broker to help me with my mortgage?

A mortgage broker may be able to help you get a lower rate. Brokers work with multiple lenders and negotiate deals on your behalf. Some brokers earn a commission from the lender. Before signing up for any broker, it is important to verify the fees.

What's the time frame to get a loan approved?

It depends on several factors including credit score, income and type of loan. It usually takes between 30 and 60 days to get approved for a mortgage.

Statistics

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

External Links

How To

How to become real estate broker

You must first take an introductory course to become a licensed real estate agent.

Next, pass a qualifying test that will assess your knowledge of the subject. This means that you will need to study at least 2 hours per week for 3 months.

You are now ready to take your final exam. You must score at least 80% in order to qualify as a real estate agent.

If you pass all these exams, then you are now qualified to start working as a real estate agent!